CSRD Unpacked: Enforcement, Compliance, and Penalties

The Corporate Sustainability Reporting Directive (CSRD) has paved the way for a new era of transparency and accountability for businesses across the

The Corporate Sustainability Reporting Directive (CSRD) has paved the way for a new era of transparency and accountability for businesses across the

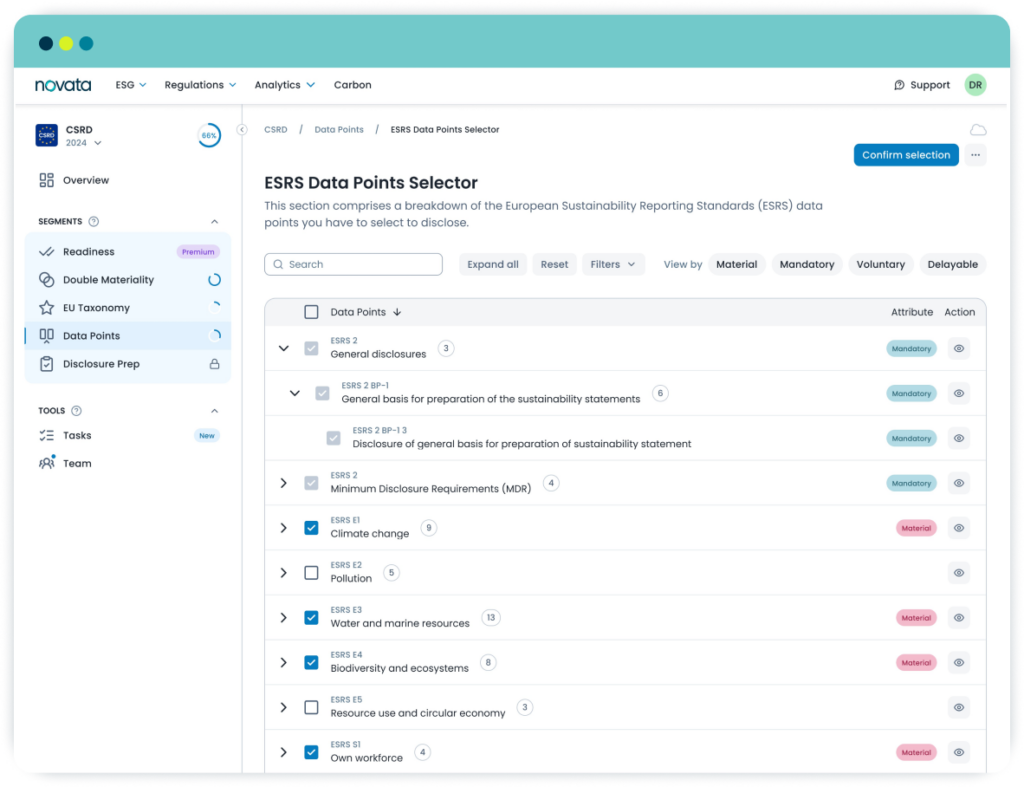

In preparing for the European Union’s Corporate Sustainability Reporting Directive (CSRD), companies must disclose impacts across environmental, social, and governance criteria. Affecting

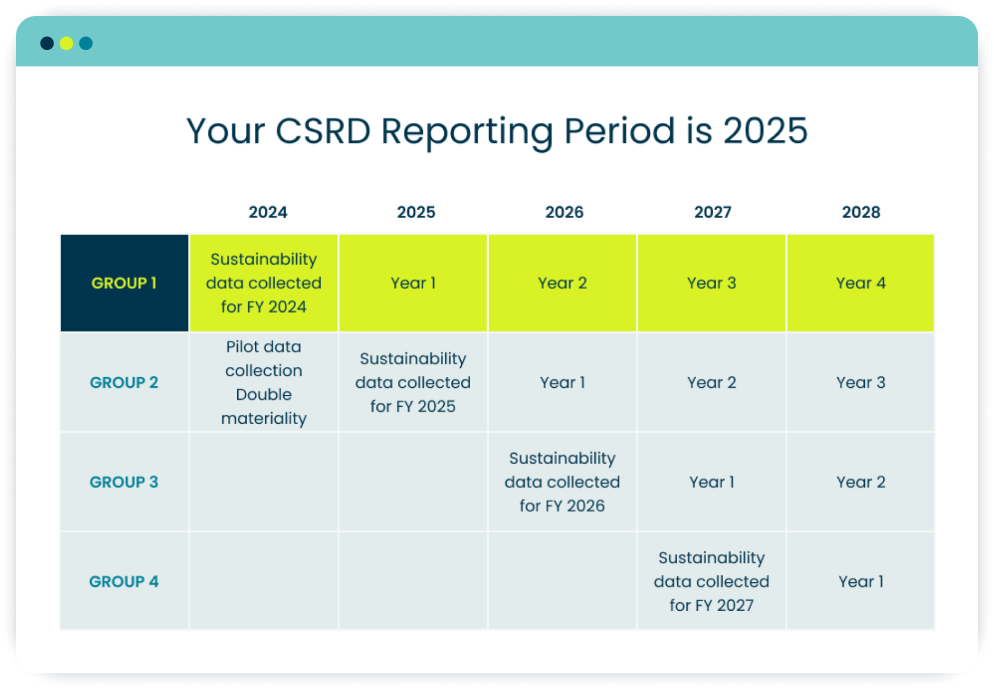

The European regulatory landscape has been a key driver of ESG adoption globally as mandatory requirements continue to shape disclosures. In the